Over the last number of years many companies received an “interesting investment opportunity” from banks that goes by the name of “DUCO”.

Before executing the DUCO, it’s important to verify the bank’s quote, so the “interesting” offer would be of interest to the firm as well.

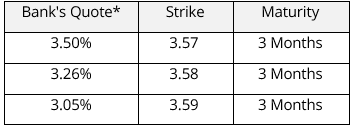

Bank’s quote of 08.02.2018:

The client makes a Dollar deposit for a specified maturity and receives a higher interest than the interest on a standard deposit for the same period, in return for the addition of the following condition: If the representative rate (BOI Fixing) on the fixing date (at 3 months) is higher than the strike, the firm will be required to convert the Dollar deposit to ILS at the strike price.

Numerical example (Reference Spot 3.4920 as of 08.02.2018):

*Annualized interest rate

Analysis of the offer:

1. Nature of the offer

The instrument offered is a structured product, which is equivalent to a Dollar deposit plus the writing of a Vanilla Call option. For example, the above offer refers to a three-month Dollar deposit and a Call option for the same period, with different strikes for which the premium is received. Therefore, the interest on the instrument is higher than that obtained from a “standard” Dollar deposit.

Implications

– The deal cannot be used as a hedge against currency movement for an exporter, since the company will not receive compensation in an event of ILS appreciation, but will only be limited as far as the FX rate received on the Dollar deposit, up to the Option’s exercise price.

– In the case of firms with a USD functional currency, the instrument creates an exposure for ILS depreciation.

– Trading the product might not be permitted according to firm’s risk management /investment policies since it includes writing a naked option.

– Periodically thereafter, if the firm is a public firm and the deposit remains in the firm’s books, the firm will be required to disclose the risks of exchange rate changes, changes in standard deviation and a change in interest rates, in accordance to Second Galai report, in its financial statements.

2. Objective pricing

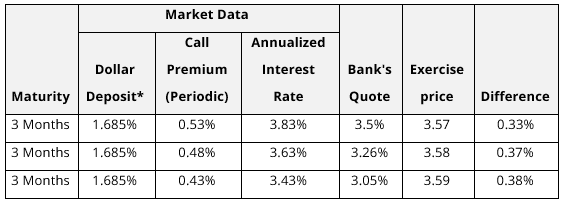

Since the product consists of a standard Dollar deposit plus a Call option, if the client is interested in trading the product, it can be constructed without the bank. Below is a comparison of prices as of 08.02.2018 (Reference Spot 3.4920)

*Interest data on standard Dollar deposits are based on indications received from clients of Financial Immunities and are dependent on the size of the deposit, the overall relationship of the client with the bank and negotiations with the bank.

• As can be seen from the above table, there is a large gap in favor of the bank

• Clients of the Financial Immunities are invited to consult with their advisors for an analysis of specific offers and, if necessary, help tailor the transactions independently.